#Functional Safety Market forecast

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Tumblr was the first site to host the blog for President Barack Obama in 2011.

Text

Functional Safety Market Demand, Analysis, Trends and Future Opportunities 2034: SPER Market Research

Functional safety is the component of safety that guarantees a system or device responds to inputs appropriately even when there are flaws. It is accomplished by the identification of possible risks, evaluation of related risks, and use of risk-reduction strategies. Functional safety is used extensively in sectors where malfunctions could cause injury, such as medical equipment, industrial automation, automotive, and aerospace. Standards like IEC 61508 (general safety) and ISO 26262 (automotive) are cited. Redundancy, fail-safe procedures, diagnostic coverage, and reliability engineering constitute key components. Minimizing failures and guaranteeing safe operation from system design to decommissioning are their goals.

According to SPER market research, ‘Global Functional Safety Market Size- By Device, By Systems, By Industry - Regional Outlook, Competitive Strategies and Segment Forecast to 2034’ state that the Global Functional Safety Market is predicted to reach 12.25 billion by 2034 with a CAGR of 6.51%.

Drivers:

The need for practical safety solutions is greatly fuelled by the growing automation of sectors including manufacturing, power generation, and oil & gas. By simplifying procedures and lowering human intervention which is essential in settings where accuracy and dependability are critical automation improves operational efficiency. The need for sophisticated functional safety systems is being greatly increased by the growth of the Industrial Internet of Things (IIoT). More devices and systems are being integrated into industrial processes via IIoT (Industrial Internet of Things) technology, which creates new challenges and possible hazards for operational safety and cyber security. In this situation, functional safety systems are essential because they are made to control and lessen these hazards by guaranteeing the safety and dependability of industrial activities.

Request a Free Sample Report: https://www.sperresearch.com/report-store/functional-safety-market?sample=1

Restraints:

Adoption may be severely hampered by the high upfront costs and complexity of putting in place functioning safety measures, especially for small and medium-sized businesses (SMEs). Furthermore, incorporating new systems into current processes can be challenging and need specific expertise and abilities that the company may not have on hand. The expense of managing and maintaining these systems is further increased by the requirement for specialist staff. These operational and financial obstacles may be too costly for many SMEs, which causes them to postpone or skip implementing functional safety systems in spite of their advantages. This disincentive effect emphasizes the necessity of affordable solutions and support systems to enable wider adoption, particularly among smaller businesses.

The global position was held by North America. The need for sophisticated functional safety solutions that can guarantee safe and dependable operations in complex environments is being driven by the growth of AI and ML applications across sectors. Some significant market players are ABB Ltd., DEKRA Group, Emerson Electric Co, Endress+Hauser Management AG, General Electric Company, HIMA Paul Hildebrandt GmbH.

For More Information, refer to below link: –

Functional Safety Market Growth

Related Reports:

Mass Flow Controller Market Growth, Size, Trends Analysis - By Type, By Flow Element, By Flow Rate, By End User- Regional Outlook, Competitive Strategies and Segment Forecast to 2034

Global Wireless Audio Device Market Growth, Size, Trends Analysis - By Product, By Technology, By Functionality, By Application- Regional Outlook, Competitive Strategies and Segment Forecast to 2034

Follow Us –

LinkedIn | Instagram | Facebook | Twitter

Contact Us:

Sara Lopes, Business Consultant — USA

SPER Market Research

+1–347–460–2899

#Functional Safety Market#Functional Safety Market Share#Functional Safety Market Size#Functional Safety Market Revenue#Functional Safety Market Analysis#Functional Safety Market Segmentation#Functional Safety Market Future Outlook#Functional Safety Market Scope#Functional Safety Market Challenges#Functional Safety Market Competition#Functional Safety Market forecast

0 notes

Text

India Pressure Cooker Market Analysis, Size, Share, Growth, Trends, and Forecasts 2023-2030

The India Pressure Cooker market has witnessed a fascinating trajectory, deeply embedded in the culinary culture of the country. This essential kitchen appliance has transcended its functional utility to become an emblematic fixture in Indian households. From the bustling streets of Delhi to the serene villages of Kerala, the pressure cooker stands as a symbol of efficiency and convenience.

Get a Free Sample Report:https://www.metastatinsight.com/request-sample/2548

Who are the largest manufacturers of the India Pressure Cooker Market worldwide?

Hawkins Cookers Limited

TTK Prestige Limited

Butterfly Gandhimathi Appliances Limited

Bajaj Electricals Limited

Stovekraft Limited

Vinod Cookware

Wonderchef Home Appliances Pvt. Ltd.

Elgi Ultra PVT LTD

Sunflame Enterprises Private Limited

Preethi Kitchen Appliances Pvt. Ltd.

Jaipan Industries Limited

United Metalik Private Limited

Bergner Group

Stahl Kitchens

Hamilton Housewares Pvt. Ltd.

In the diverse tapestry of Indian cuisine, where flavors dance with complexity, the pressure cooker emerges as a stalwart companion. Its significance goes beyond the mundane act of cooking; it represents a seamless fusion of tradition and modernity. The rhythmic hiss of steam escaping the pressure cooker has become a reassuring melody, echoing across the kitchens of millions.

Access Full Report @https://www.metastatinsight.com/report/india-pressurecooker-market

The Indian market for pressure cookers is not a mere aggregation of products but a reflection of the diverse preferences and culinary practices that span the length and breadth of the nation. From the compact kitchens of urban apartments to the sprawling setups in rural households, pressure cookers have found their place, adapting to the unique needs of each setting.

This market is not just about metal vessels and rubber gaskets; it’s a testament to innovation. As the demands of the modern consumer evolve, pressure cookers have metamorphosed into sophisticated appliances equipped with advanced features. Digital controls, safety mechanisms, and energy-efficient designs are seamlessly integrated into these culinary workhorses, ensuring they keep pace with the dynamic lifestyle of today’s Indian consumer.

Moreover, the market has seen a surge in eco-conscious designs, with manufacturers increasingly focusing on sustainability. Materials are carefully chosen, and production processes are streamlined to minimize environmental impact. This reflects a growing awareness among both manufacturers and consumers about the need for responsible and sustainable practices.

The India Pressure Cooker market is not just about meeting functional needs; it is a vibrant ecosystem where tradition meets innovation, where utility meets aesthetics. From the aromatic biryanis of Lucknow to the spicy curries of Chennai, pressure cookers have become an integral part of the gastronomic narrative, shaping the way India cooks and savors its diverse culinary delights. In the heart of this market, lies not just an appliance, but a cultural artifact that binds generations, bridging the gap between tradition and modernity in the Indian kitchen.

India Pressure Cooker market is estimated to reach $611.3 Million by 2031; growing at a CAGR of 8.9% from 2024 to 2031.

Contact Us:

+1 214 613 5758

#IndiaPressureCooker#IndiaPressureCookerMarket#IndiaPressureCookerindustry#marketsize#marketgrowth#marketforecast#marketanalysis#marketdemand#marketreport#marketresearch

2 notes

·

View notes

Text

Aquatic Robot Market to Eyewitness Huge Growth by 2030

Latest business intelligence report released on Global Aquatic Robot Market, covers different industry elements and growth inclinations that helps in predicting market forecast. The report allows complete assessment of current and future scenario scaling top to bottom investigation about the market size, % share of key and emerging segment, major development, and technological advancements. Also, the statistical survey elaborates detailed commentary on changing market dynamics that includes market growth drivers, roadblocks and challenges, future opportunities, and influencing trends to better understand Aquatic Robot market outlook. List of Key Players Profiled in the study includes market overview, business strategies, financials, Development activities, Market Share and SWOT analysis: Atlas Maridan ApS. (Germany), Deep Ocean Engineering Inc. (United States), Bluefin Robotics Corporation (United States), ECA SA (France), International Submarine Engineering Ltd. (Canada), Inuktun Services Ltd. (Canada), Oceaneering International, Inc. (United States), Saab Seaeye (Sweden), Schilling Robotics, LLC (United States), Soil Machine Dynamics Ltd. (United Kingdom) Download Free Sample PDF Brochure (Including Full TOC, Table & Figures) @ https://www.advancemarketanalytics.com/sample-report/177845-global-aquatic-robot-market Brief Overview on Aquatic Robot: Aquatic robots are those that can sail, submerge, or crawl through water. They can be controlled remotely or autonomously. These robots have been regularly utilized for seafloor exploration in recent years. This technology has shown to be advantageous because it gives enhanced data at a lower cost. Because underwater robots are meant to function in tough settings where divers' health and accessibility are jeopardized, continuous ocean surveillance is extended to them. Maritime safety, marine biology, and underwater archaeology all use aquatic robots. They also contribute significantly to the expansion of the offshore industry. Two important factors affecting the market growth are the increased usage of advanced robotics technology in the oil and gas industry, as well as increased spending in defense industries across various countries. Key Market Trends: Growth in AUV Segment Opportunities: Adoption of aquatic robots in military & defense

Increased investments in R&D activities Market Growth Drivers: Growth in adoption of automated technology in oil & gas industry

Rise in awareness of the availability of advanced imaging system Challenges: Required highly skilled professional for maintenance Segmentation of the Global Aquatic Robot Market: by Type (Remotely Operated Vehicle (ROV), Autonomous Underwater Vehicles (AUV)), Application (Defense & Security, Commercial Exploration, Scientific Research, Others) Purchase this Report now by availing up to 10% Discount on various License Type along with free consultation. Limited period offer. Share your budget and Get Exclusive Discount @: https://www.advancemarketanalytics.com/request-discount/177845-global-aquatic-robot-market Geographically, the following regions together with the listed national/local markets are fully investigated: • APAC (Japan, China, South Korea, Australia, India, and Rest of APAC; Rest of APAC is further segmented into Malaysia, Singapore, Indonesia, Thailand, New Zealand, Vietnam, and Sri Lanka) • Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe; Rest of Europe is further segmented into Belgium, Denmark, Austria, Norway, Sweden, The Netherlands, Poland, Czech Republic, Slovakia, Hungary, and Romania) • North America (U.S., Canada, and Mexico) • South America (Brazil, Chile, Argentina, Rest of South America) • MEA (Saudi Arabia, UAE, South Africa)Furthermore, the years considered for the study are as follows: Historical data – 2017-2022 The base year for estimation – 2022 Estimated Year – 2023 Forecast period** – 2023 to 2028 [** unless otherwise stated] Browse Full in-depth TOC @: https://www.advancemarketanalytics.com/reports/177845-global-aquatic-robot-market

Summarized Extracts from TOC of Global Aquatic Robot Market Study Chapter 1: Exclusive Summary of the Aquatic Robot market Chapter 2: Objective of Study and Research Scope the Aquatic Robot market Chapter 3: Porters Five Forces, Supply/Value Chain, PESTEL analysis, Market Entropy, Patent/Trademark Analysis Chapter 4: Market Segmentation by Type, End User and Region/Country 2016-2027 Chapter 5: Decision Framework Chapter 6: Market Dynamics- Drivers, Trends and Challenges Chapter 7: Competitive Landscape, Peer Group Analysis, BCG Matrix & Company Profile Chapter 8: Appendix, Methodology and Data Source Buy Full Copy Aquatic RobotMarket – 2021 Edition @ https://www.advancemarketanalytics.com/buy-now?format=1&report=177845 Contact US : Craig Francis (PR & Marketing Manager) AMA Research & Media LLP Unit No. 429, Parsonage Road Edison, NJ New Jersey USA – 08837 Phone: +1 201 565 3262, +44 161 818 8166 [email protected]

#Global Aquatic Robot Market#Aquatic Robot Market Demand#Aquatic Robot Market Trends#Aquatic Robot Market Analysis#Aquatic Robot Market Growth#Aquatic Robot Market Share#Aquatic Robot Market Forecast#Aquatic Robot Market Challenges

2 notes

·

View notes

Text

Melamine Market is Expected to Grow at a CAGR of 3.87% during the forecast period until 2032

The melamine market has witnessed remarkable growth and diversification in recent years, propelled by a myriad of factors shaping the global landscape. Melamine, a nitrogen-rich organic compound, finds extensive applications across various industries, including construction, automotive, textiles, packaging, and food service. Its unique properties, such as high flame resistance, thermal stability, durability, and chemical inertness, have made melamine a versatile and indispensable material in numerous manufacturing processes and end-use applications.

One of the primary drivers of the melamine market is the increasing demand from the construction industry. Melamine-based products, such as melamine formaldehyde resins and melamine foam insulation, are widely used in construction applications such as laminates, decorative panels, flooring, countertops, and insulation materials. With rapid urbanization, infrastructure development, and construction activities on the rise globally, the demand for melamine-based construction materials is expected to surge.

Read Full Report: https://www.chemanalyst.com/industry-report/melamine-market-812

Moreover, the automotive sector represents another significant market for melamine, driven by the increasing demand for lightweight, durable, and aesthetically appealing materials. Melamine-based components, such as automotive interior trim, dashboard panels, door panels, and decorative parts, offer excellent properties such as scratch resistance, color stability, and surface finish, thereby enhancing the overall aesthetics and functionality of vehicles. As automotive manufacturers focus on improving fuel efficiency, reducing emissions, and enhancing passenger comfort and safety, the demand for melamine-based automotive materials is projected to grow substantially.

Furthermore, the textiles industry presents lucrative opportunities for the melamine market, particularly in the manufacturing of melamine-formaldehyde resins for textile finishing and coating applications. Melamine resins impart crease resistance, wrinkle resistance, and color fastness to textiles, thereby enhancing their durability, appearance, and performance. With the growing demand for high-quality textiles, home furnishings, and apparel, the demand for melamine-based textile additives is expected to increase.

Additionally, the packaging industry represents a significant market for melamine, driven by the rising demand for lightweight, durable, and eco-friendly packaging materials. Melamine-based products, such as melamine-formaldehyde resins and melamine foam packaging, offer excellent properties such as thermal insulation, moisture resistance, and shock absorption, making them ideal for packaging applications such as food packaging, electronics packaging, and industrial packaging. As consumers increasingly prioritize sustainability, recyclability, and environmental friendliness, the demand for melamine-based packaging solutions is expected to grow.

Despite the promising outlook, the melamine market faces challenges and constraints, including fluctuating raw material prices, regulatory compliance issues, and environmental concerns related to formaldehyde emissions. However, industry stakeholders are actively addressing these challenges through initiatives focused on product innovation, sustainability, and regulatory compliance. Moreover, strategic partnerships, mergers, and acquisitions are driving consolidation and market expansion in the melamine industry.

In conclusion, the melamine market is poised for continued growth and innovation, driven by its versatile applications, inherent properties, and compatibility with evolving market trends. By leveraging its strengths in construction, automotive, textiles, packaging, and other sectors, the melamine market can navigate towards a more sustainable and prosperous future, ensuring its relevance and competitiveness in the global marketplace.

About us:

ChemAnalyst is an online platform offering a comprehensive range of market analysis and pricing services, as well as up-to-date news and deals from the chemical and petrochemical industry, globally.

Being awarded ‘The Product Innovator of the Year, 2023’, ChemAnalyst is an indispensable tool for navigating the risks of today's ever-changing chemicals market.

The platform helps companies strategize and formulate their chemical procurement by tracking real time prices of more than 400 chemicals in more than 25 countries.

ChemAnalyst also provides market analysis for more than 1000 chemical commodities covering multifaceted parameters including Production, Demand, Supply, Plant Operating Rate, Imports, Exports, and much more. The users will not only be able to analyse historical data but will also get to inspect detailed forecasts for upto 10 years. With access to local field teams, the company provides high-quality, reliable market analysis data for more than 40 countries.

Contact us:

420 Lexington Avenue, Suite 300

New York, NY

United States, 10170

Email-id: [email protected]

Mobile no: +1-3322586602

#Melamine#Melaminemarket#Melaminemarketsize#Melaminemarkettrends#Melaminemarketgrowth#Melaminemarketshare#Melaminedemand

2 notes

·

View notes

Text

Notchback Market Set to Reach New Heights: Market Overview, Key Trends, Porter's Analysis, and Key Takeaways

Notchback Market

Market Overview: The global Notchback Market is estimated to be valued at US$78.49 billion in 2023, with a projected compound annual growth rate (CAGR) of 5% from 2023 to 2030. A notchback refers to a car body style with a distinct rear deck lid that is positioned higher than the trunk. These vehicles offer valuable advantages to consumers, including spaciousness, practicality, and improved aerodynamics. Notchbacks cater to the needs of various consumers who prioritize functionality and efficiency without compromising on style. These vehicles provide ample cargo space while maintaining an elegant and sleek design. With the growing demand for versatile vehicles that combine form and function, the notchback segment is expected to witness substantial growth in the coming years. Market Key Trends: One key trend shaping the Notchback Market is the focus on sustainability and electric mobility. As environmental concerns rise and governments push for stricter emission regulations, automakers are increasingly investing in electric vehicles (EVs) within the notchback segment. For instance, key players like Volkswagen Group, BMW Group, and Mercedes-Benz are launching electric notchback models to meet evolving consumer demands and contribute to a sustainable future. The integration of advanced technologies is another significant trend driving the notchback market. Features such as advanced driver-assistance systems (ADAS), connectivity solutions, and enhanced safety features are becoming increasingly prevalent in notchback vehicles. These technological advancements enhance the driving experience and provide a competitive edge to automakers. Porter's Analysis: - Threat of New Entrants: The threat of new entrants in the notchback market is relatively low due to significant capital requirements, established brand presence of key players, and complex manufacturing processes.

- Bargaining Power of Buyers: Buyers in the notchback market have moderate bargaining power as they have access to various options from different manufacturers. However, their power is somewhat limited due to the innovation and brand loyalty associated with established automakers.

- Bargaining Power of Suppliers: Suppliers who provide key components such as engines, transmissions, and electronics have moderate bargaining power due to the presence of multiple automakers as their potential customers. - Threat of New Substitutes: The threat of new substitutes for notchback vehicles is low, as no alternative body style offers the same combination of style, functionality, and aerodynamics.

- Competitive Rivalry: Competitive rivalry among key players in the notchback market is intense, as established automakers constantly strive to innovate, offer unique features, and expand their market presence. Key Takeaways: 1: The global notchback market is expected to witness high growth, exhibiting a CAGR of 5% over the forecast period, fueled by increasing consumer demand for spacious, practical, and aerodynamically efficient vehicles. This growth will be driven by the emphasis on sustainability and electric mobility. 2: The fastest-growing and dominating region in the notchback market is likely to be North America, with rising consumer preferences for vehicles that balance functionality and elegance, as well as stringent emission regulations driving the adoption of electric notchback cars. 3: Key players operating in the global notchback market include Volkswagen Group, BMW Group, Mercedes-Benz (Daimler AG), Audi (Volkswagen Group), Ford Motor Company, General Motors, Toyota Motor Corporation, Honda Motor Co. Ltd., Hyundai Motor Group, Kia Motors Corporation, Nissan Motor Co. Ltd., Mazda Motor Corporation, Subaru Corporation, Volvo Cars, and Peugeot SA. These industry leaders are at the forefront of innovation, investing in electric mobility and incorporating advanced technologies to meet consumer expectations. In conclusion, the notchback market is poised for significant growth as automakers focus on sustainability, integrate advanced technologies, and cater to consumer demands for spacious and aerodynamically efficient vehicles. With key players leading the way, the notchback segment promises to offer consumers a perfect blend of practicality, style, and sustainable mobility options in the years to come.

#Notchback Market Market Overview#Notchback Market Market Key Trends#Notchback Market Porter's Analysis#Notchback Market Key Takeaways

2 notes

·

View notes

Text

Workwear/Uniforms (Uniforms & Workwear’s) Market Forecast 2024 to 2032

Workwear, also known as uniforms or work clothes, refers to specialized clothing worn by employees in various industries and professions. These garments are designed to provide safety, functionality, and a professional appearance while performing job-related tasks. Workwear serves multiple purposes, including protection from workplace hazards, identification of employees, and adherence to industry standards.

The Workwear/Uniforms (Uniforms & Workwear’s) Market was valued at USD 579.80 Million in 2022 and is expected to register a CAGR of 3.96% by 2032.

Occupational safety regulations mandate the use of specific workwear to protect employees from hazards in various industries, such as construction, manufacturing, and healthcare. Compliance with safety standards drives the demand for appropriate workwear.

Get a Free Sample Pdf

2 notes

·

View notes

Text

Ion Exchange Resins Market Outlook: Forecasting Growth from 2025 to 2035

The ion exchange resins market, historically dominated by applications in municipal water treatment, pharmaceutical purification, and food processing, is now undergoing a pivotal transformation. A specialized subsegment—nuclear-grade ion exchange resins—is witnessing increased demand, fueled by the global shift toward cleaner, low-carbon nuclear energy and the accelerated deployment of Small Modular Reactors (SMRs).

The Strategic Role of Nuclear-Grade Ion Exchange Resins

Unlike standard resins used in water softening, nuclear-grade resins are engineered for high-radiation, high-temperature environments and must comply with stringent purity and safety standards. These resins play an indispensable role in nuclear operations, including:

Purification of reactor coolant systems

Decontamination of spent fuel pools

Treatment of radioactive wastewater

Their ability to remove radioactive isotopes like cesium-137, strontium-90, and cobalt-60 ensures operational safety and regulatory compliance in nuclear facilities.

A notable example of their critical use was during the Fukushima Daiichi nuclear crisis, where emergency deployment of nuclear-grade resins helped mitigate contamination.

𝐌𝐚𝐤𝐞 𝐈𝐧𝐟𝐨𝐫𝐦𝐞𝐝 𝐃𝐞𝐜𝐢𝐬𝐢𝐨𝐧𝐬 – 𝐀𝐜𝐜𝐞𝐬𝐬 𝐘𝐨𝐮𝐫 𝐒𝐚𝐦𝐩𝐥𝐞 𝐑𝐞𝐩𝐨𝐫𝐭 𝐈𝐧𝐬𝐭𝐚𝐧𝐭𝐥𝐲! https://www.futuremarketinsights.com/reports/sample/rep-gb-1001

Market Outlook and Growth Forecast

According to Future Market Insights, the ion exchange resins market is projected to grow from USD 1,617.6 million in 2025 to USD 2,609.9 million by 2035, expanding at a CAGR of 4.9%. This steady growth is being driven not just by water treatment, but increasingly by:

The expansion of nuclear infrastructure worldwide

Increased use of ion exchange systems in radioactive waste management

Growth of SMRs and other advanced reactor technologies

Key Takeaways

High-performance niche: Nuclear-grade resins are built for environments where failure is not an option.

Strategic supply constraints: Only a few global suppliers (e.g., Purolite, LANXESS, Thermax) are certified for nuclear-grade resin production.

Geopolitical risk: Trade disputes and raw material dependency (styrene, divinylbenzene) threaten stable supply.

Local innovation: India and the U.S. are investing in domestic manufacturing and research on composite resins.

Shifting procurement models: Utilities are moving toward long-term resin supply and service contracts.

Supply Chain and Regulatory Challenges

The production of nuclear-grade ion exchange resins requires pharmaceutical-grade manufacturing environments, ISO and NRC/IAEA certifications, and years of regulatory alignment. Furthermore, geopolitical tensions—such as the 2023 EU-China trade dispute—have exposed vulnerabilities in global resin supply chains.

These challenges make rapid scaling difficult, increasing the market’s reliance on a few certified producers.

𝐔𝐧𝐥𝐨𝐜𝐤 𝐂𝐨𝐦𝐩𝐫𝐞𝐡𝐞𝐧𝐬𝐢𝐯𝐞 𝐌𝐚𝐫𝐤𝐞𝐭 𝐈𝐧𝐬𝐢𝐠𝐡𝐭𝐬 – 𝐄𝐱𝐩𝐥𝐨𝐫𝐞 𝐭𝐡𝐞 𝐅𝐮𝐥𝐥 𝐑𝐞𝐩𝐨𝐫𝐭 𝐍𝐨𝐰: https://www.futuremarketinsights.com/reports/ion-exchange-resins-market

Innovation and Localization as Strategic Priorities

To secure supply and reduce import dependence, several governments are promoting local production of nuclear-grade resins. In India, the Department of Atomic Energy has collaborated with domestic manufacturers, achieving successful deployment in facilities like the Tarapur Atomic Power Station.

Simultaneously, the U.S. Department of Energy is investing in next-gen resin materials enhanced with inorganic nanoparticles, aiming for improved durability, radiation resistance, and performance longevity.

Looking Ahead: A Market of Strategic Importance

The importance of ion exchange resins—especially those for nuclear use—extends beyond their technical function. They are becoming a strategic commodity essential for national energy security, waste management, and regulatory compliance.

As countries embrace nuclear energy as part of their net-zero emissions roadmap, the demand for high-performance, reliable resins will continue to reshape the global ion exchange market landscape.

0 notes

Text

Ready To Drink (RTD) Tea Market: Applications and Regional Insights During the Forecasted Period 2025 to 2035

The Ready to Drink (RTD) Tea Market is poised for substantial growth over the next decade. It is anticipated to reach USD 40,007.5 million by 2025 and expand further to USD 88,802.7 million by 2035, recording a robust CAGR of 8.3% during the forecast period.

The market's momentum is driven by the introduction of innovative tea varieties such as organic and herbal options, along with advancements in convenient packaging and wider retail availability. Between 2025 and 2035, the RTD tea industry is expected to witness sustained growth as consumers increasingly seek convenient, healthy beverage alternatives. Rising awareness about the health benefits of tea, combined with the popularity of functional and herbal teas and the demand for low-sugar beverages, is expanding the consumer base.

RTD tea appeals across demographics, particularly in urban areas and among health-conscious consumers. 𝗦t𝗮𝘆 𝗜𝗻𝗳𝗼𝗿𝗺𝗲𝗱 – 𝗥𝗲𝗾𝘂𝗲𝘀t. 𝗮 𝗦𝗮𝗺𝗽𝗹𝗲 𝗖𝗼𝗽𝘆 𝗳𝗼𝗿 𝗘𝘅𝗰𝗹𝘂𝘀𝗶𝘃𝗲 𝗜𝗻𝘀𝗶𝗴𝗵t𝘀: https://www.futuremarketinsights.com/reports/sample/rep-gb-14341 𝗞𝗲𝘆 𝗥𝗲𝗮𝗱𝘆 t𝗼 𝗗𝗿𝗶𝗻𝗸 (𝗥𝗧𝗗) 𝗧𝗲𝗮 𝗠𝗮𝗿𝗸𝗲t 𝗧𝗿𝗲𝗻𝗱𝘀 𝗛𝗶𝗴𝗵𝗹𝗶𝗴𝗵t𝗲𝗱 • Demand for Organic and Herbal RTD Teas: Clean-label and natural ingredient preferences are influencing purchasing decisions. • Shift Toward Low-Sugar and Functional Beverages: Consumers are choosing teas that offer added health benefits, like adaptogens and probiotics. • Premiumization and Craft Beverages: There is growing interest in high-end, artisanal RTD teas featuring unique flavor profiles. • Eco-Friendly Packaging: Sustainable packaging innovations are becoming a major competitive differentiator.

• Expansion of E-commerce Channels: Online platforms are helping brands reach wider audiences, especially with specialty and wellness teas. 𝗥𝗲𝗮𝗱𝘆 t𝗼 𝗗𝗿𝗶𝗻𝗸 (𝗥𝗧𝗗) 𝗧𝗲𝗮 𝗜𝗻𝗱𝘂𝘀t𝗿𝘆 𝗗𝗲𝘃𝗲𝗹𝗼𝗽𝗺𝗲𝗻t𝘀 The industry is witnessing new product launches emphasizing health and wellness benefits. Major players are focusing on herbal, unsweetened, and functional RTD teas to meet changing consumer demands.

Additionally, collaborations between tea brands and sustainable packaging companies are enhancing market appeal. Companies are investing in regional expansion and premium product lines to strengthen their foothold globally. 𝗞𝗲𝘆 𝗧𝗮𝗸𝗲𝗮𝘄𝗮𝘆𝘀 𝗼𝗳 𝗥𝗲𝗽𝗼𝗿t. • The global RTD tea market is projected to grow at a CAGR of 8.3% from 2025 to 2035. • Organic, herbal, and functional RTD teas are the fastest-growing segments. • Sustainable packaging and clean-label products are becoming central to brand strategies. • Urbanization and busy lifestyles are driving the need for convenient beverage options. 𝗥𝗲𝗮𝗱𝘆 t𝗼 𝗗𝗿𝗶𝗻𝗸 (𝗥𝗧𝗗) 𝗧𝗲𝗮 𝗠𝗮𝗿𝗸𝗲t 𝗗𝗿𝗶𝘃𝗲𝗿𝘀 • Health Consciousness: Increasing awareness about the health benefits of tea, especially green tea, herbal infusions, and adaptogen-rich options, is a major market driver. • Demand for Convenience: Busy consumers prefer ready-to-consume beverages that fit into their fast-paced lifestyles. • Innovation in Flavors and Formats: The launch of exotic flavors, limited editions, and cold-brew varieties is capturing consumer interest. • Sustainability Trends: Environmental concerns are pushing both consumers and companies toward eco-friendly, recyclable packaging. 𝗔𝗰𝗰𝗲𝘀𝘀 𝗙𝘂𝗹𝗹 𝗥𝗲𝗽𝗼𝗿t: https://www.futuremarketinsights.com/reports/ready-to-drink-rtd-tea-market 𝗥𝗲𝗮𝗱𝘆 to 𝗗𝗿𝗶𝗻𝗸 (𝗥𝗧𝗗) 𝗧𝗲𝗮 𝗠𝗮𝗿𝗸𝗲t 𝗥𝗲𝗴𝗶𝗼𝗻𝗮𝗹 𝗜𝗻𝘀𝗶𝗴𝗵t𝘀 United States The RTD tea market in the United States is expanding steadily, with consumers increasingly seeking healthier beverage options. Natural and organic RTD teas are particularly popular, supported by strict food safety and organic certification standards from bodies like the FDA and USDA. Trends such as low-sugar, functional beverages, and artisanal tea products are gaining ground. Investment in eco-friendly packaging and plant-based formulations is accelerating.

The U.S. RTD tea market is projected to grow at a CAGR of 8.5% between 2025 and 2035. United Kingdom The RTD tea sector in the UK is thriving thanks to a growing demand for convenient and health-focused beverages. Consumers are gravitating towards premium organic and herbal tea drinks, while regulatory agencies like the Food Standards Agency promote lower sugar levels and sustainable practices. Cold-brew, herbal infusions, and naturally sweetened teas are prominent trends. Focus on eco-friendly packaging and innovative flavors continues to drive market growth.

The UK's RTD tea market is forecasted to expand at a CAGR of 8.1%. European Union The EU market for RTD tea is experiencing strong growth, led by the rising demand for organic, natural, and fortified beverages. Regulations promoting reduced sugar content and transparency in labeling are shaping market dynamics. Germany, France, and the Netherlands are among the leading countries, with high interest in wellness beverages and high-end tea varieties. Green tea and matcha-based RTD products are becoming consumer favorites.

The EU RTD tea market is expected to grow at a CAGR of 8.2%. Japan Japan’s RTD tea market continues its rapid evolution, with a strong cultural affinity for tea driving innovation. Traditional and modern herbal teas, especially unsweetened variants, are in high demand.

Regulatory bodies like the MHLW and CAA oversee product quality and labeling. Trends such as bottled green and barley tea, teas enriched with collagen and probiotics, and sustainable packaging solutions are shaping the market. Japan’s RTD tea market is anticipated to grow at a CAGR of 8.4%. South Korea In South Korea, RTD tea consumption is rising quickly, fueled by an increasing preference for healthy, convenient drinks. Traditional herbal teas and high-end specialty teas are gaining popularity, supported by regulations from the Korean Food and Drug Administration. The popularity of ginseng, barley, and probiotic-enriched RTD teas is soaring. The market is also benefitting from strong online and retail distribution networks.

South Korea’s RTD tea market is forecast to grow at a CAGR of 8.3%. 𝗖𝗼𝗺𝗽𝗲t𝗶t𝗶𝗼𝗻 𝗢𝘂t𝗹𝗼𝗼𝗸 The global RTD tea market is highly competitive, with key players focusing on innovation, premiumization, and sustainability to gain a competitive edge. Major brands are investing in organic formulations, functional benefits, and regional flavor preferences to differentiate their offerings.

Mergers, acquisitions, and partnerships are common strategies to expand market reach and strengthen product portfolios. Leading players include Nestlé S.A., PepsiCo Inc., The Coca-Cola Company, Arizona Beverage Company, and Unilever PLC, among others. Startups and niche brands specializing in functional and artisanal RTD teas are also reshaping the competitive landscape. 𝗘𝘅𝗽𝗹𝗼𝗿𝗲 𝗕𝗲𝘃𝗲𝗿𝗮𝗴𝗲𝘀 𝗜𝗻𝗱𝘂𝘀t𝗿𝘆 𝗔𝗻𝗮𝗹𝘆𝘀𝗶𝘀: www.futuremarketinsights.com/industr…/beverages 𝗥𝗲𝗮𝗱𝘆 𝗧𝗼 𝗗𝗿𝗶𝗻𝗸 (𝗥𝗧𝗗) 𝗧𝗲𝗮 𝗠𝗮𝗿𝗸𝗲t 𝗦𝗲𝗴𝗺𝗲𝗻t𝗮t𝗶𝗼𝗻 By Product Types: • Herbal • Black tea • Green tea • Others By Sales Channel: • Direct Sales • Indirect Sales By Region: • North America • Latin America • Western Europe • Eastern Europe • East Asia • South Asia Pacific • Middle East and Africa

0 notes

Text

global Video Sync Separator Market Industry Outlook: Trends and Forecasts

MARKET INSIGHTS

The global Video Sync Separator Market size was valued at US$ 234 million in 2024 and is projected to reach US$ 312 million by 2032, at a CAGR of 4.1% during the forecast period 2025-2032

Video sync separators are semiconductor devices designed to extract synchronization signals (horizontal and vertical timing information) from composite video inputs. These components are critical in processing video signals across multiple standards, including NTSC, PAL, SECAM, SDTV, and HDTV. By isolating sync pulses, they enable stable video display and synchronization in applications such as broadcasting, imaging, and consumer electronics.

The market is expanding due to rising demand for high-definition video processing, particularly in surveillance systems and digital displays. While the U.S. dominates with an estimated market size of USD 12.4 million in 2024, China is expected to witness accelerated growth, driven by increasing electronics manufacturing. Key players like Texas Instruments, Renesas, and ROHM collectively hold over 60% of the global market share, with innovations in low-power and multi-standard compatibility shaping competition.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Video Processing Applications in Consumer Electronics to Accelerate Market Growth

The global video sync separator market is experiencing robust growth, primarily driven by the surging demand for high-quality video processing solutions in consumer electronics such as televisions, gaming consoles, and multimedia devices. Video sync separators play an integral role in extracting synchronization signals from complex video inputs, ensuring seamless display performance. With the rising adoption of 4K and 8K displays, the need for advanced synchronization solutions has become more critical than ever. The market is expected to witness a compound annual growth rate of over 6% from 2024 to 2032, fueled by these technological advancements.

Growth in Surveillance and Imaging Applications to Boost Demand

The surveillance industry’s rapid expansion is creating significant opportunities for video sync separator manufacturers. Modern security systems increasingly rely on high-definition video processing capabilities to deliver clear and stable images. Video sync separators enable precise synchronization in multi-camera setups, which is essential for traffic monitoring, public safety, and commercial security applications. The global surveillance camera market, valued at approximately $50 billion in 2024, continues to grow at a steady pace, directly benefiting the video sync separator segment.

Furthermore, medical imaging equipment manufacturers are incorporating advanced video processing solutions to enhance diagnostic accuracy. The integration of video sync separators in ultrasound machines, endoscopes, and other medical imaging devices is expected to drive substantial market growth in the healthcare sector.

MARKET RESTRAINTS

Declining Demand for Legacy Video Standards to Limit Market Expansion

While the video sync separator market shows promising growth potential, the gradual phasing out of legacy video standards presents a significant challenge. Analog video formats such as NTSC and PAL, which once dominated the market, are being replaced by digital interfaces like HDMI and DisplayPort. This transition reduces the need for traditional sync separation solutions in modern devices. Manufacturers face the challenge of adapting their product portfolios to remain relevant in an increasingly digital ecosystem.

Other Restraints

Integration Complexities in Advanced Systems Modern video processing systems require complex integration of multiple functionalities, making it challenging to implement standalone sync separator chips. System-on-chip (SoC) solutions that incorporate synchronization functions directly are becoming more prevalent, potentially reducing demand for discrete video sync separator components.

Price Pressure in Mature Segments The consumer electronics sector, particularly in emerging markets, remains highly price-sensitive. Intense competition among manufacturers often leads to margin compression, making it difficult to maintain profitability in standard-definition video processing solutions.

MARKET OPPORTUNITIES

Emerging Applications in Automotive Displays to Create New Growth Avenues

The automotive industry presents significant opportunities for video sync separator manufacturers, driven by the increasing adoption of advanced driver assistance systems (ADAS) and in-vehicle infotainment solutions. Modern vehicles incorporate multiple high-resolution displays for navigation, entertainment, and vehicle diagnostics, all requiring precise video synchronization. The automotive display market is projected to grow at nearly 8% annually through 2030, creating substantial demand for specialized video processing components.

Additionally, the development of augmented reality head-up displays (AR HUDs) in premium vehicles requires advanced synchronization capabilities to ensure seamless integration of digital information with the real-world view. This emerging technology segment is expected to drive innovation in video sync separator solutions.

MARKET CHALLENGES

Rapid Technological Evolution Requires Continuous R&D Investment

The video processing industry faces constant technological disruption, requiring manufacturers to maintain significant research and development expenditures. Developing solutions that support emerging video standards while maintaining backward compatibility with legacy systems presents both technical and financial challenges. Smaller players in particular may struggle to keep pace with the innovation required to remain competitive.

Other Challenges

Supply Chain Vulnerabilities The global semiconductor shortage highlighted the fragility of electronics supply chains. Video sync separator manufacturers must navigate component availability issues and price fluctuations that can impact production schedules and profitability.

Standardization Gaps The lack of unified standards for emerging video interfaces creates compatibility challenges. Developing solutions that work seamlessly across different manufacturers’ implementations requires extensive testing and adaptation efforts.

VIDEO SYNC SEPARATOR MARKET TRENDS

Rising Demand for High-Quality Video Processing in Consumer Electronics

The global video sync separator market is experiencing significant growth driven by increasing adoption in consumer electronics, particularly in televisions, gaming consoles, and video capture devices. With the global consumer electronics sector projected to surpass $1.5 trillion by 2030, manufacturers are prioritizing enhanced video processing capabilities to meet consumer expectations for pristine image quality. Sync separators play a critical role in extracting precise timing signals from composite video streams, ensuring stable synchronization across various display technologies. Recent advancements in 4K and 8K resolution standards have further amplified demand for high-precision sync separation chips capable of handling ultra-high-definition signals without artifact generation.

Other Trends

Integration with Emerging Display Technologies

As next-generation display technologies gain traction in the automotive and industrial sectors, video sync separators are evolving to support novel applications. The automotive display market alone is expected to grow at a CAGR of 8% through 2030, creating substantial opportunities for sync separator suppliers. Modern heads-up displays and advanced driver assistance systems (ADAS) require robust synchronization solutions that maintain performance across extreme temperature ranges and electromagnetic interference conditions. Leading manufacturers are responding with specialized automotive-grade sync separators featuring enhanced noise immunity and wider operating voltage ranges.

Medical Imaging Applications Driving Innovation

The medical imaging sector represents one of the fastest-growing applications for video sync separators, with the global medical displays market anticipated to reach $3.2 billion by 2027. Diagnostic imaging equipment such as endoscopes, ultrasound machines, and surgical displays demand ultra-reliable sync separation to maintain critical video feeds during medical procedures. This has prompted development of medical-grade sync separators with features like automatic format detection, minimum jitter generation, and redundant synchronization pathways. The trend toward minimally invasive surgery and telemedicine is further accelerating adoption of these specialized components in healthcare settings worldwide.

Video Sync Separator Market

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation Drives Competition in the Video Sync Separator Space

The global Video Sync Separator market, valued at $XX million in 2024, exhibits a semi-fragmented competitive landscape with established semiconductor giants competing alongside specialized component manufacturers. Renesas Electronics Corporation emerges as a market leader, leveraging its extensive expertise in analog and mixed-signal ICs to capture significant market share. The company’s advanced sync separator ICs supporting multiple video standards give it a strong position in both consumer electronics and professional imaging applications.

Texas Instruments and ROHM Semiconductor represent other major players, collectively accounting for a substantial portion of 2024’s global revenue. Texas Instruments’ broad portfolio of video interface solutions, combined with its strong distribution network, positions it well in North American and European markets. Meanwhile, ROHM has strengthened its market position through specialized low-power solutions favored in portable electronics.

Medium-sized players like Maxim Integrated (now part of Analog Devices) and Intersil (acquired by Renesas) have carved out specialized niches through innovative product designs. These companies compete on performance parameters such as jitter reduction and multi-standard compatibility, particularly in high-end broadcast and medical imaging applications.

Recent industry movements show increasing R&D investment in next-generation video processing technologies. Several key players are expanding their product lines to address emerging standards and higher resolution requirements in display technologies. Strategic partnerships between semiconductor manufacturers and display system integrators are becoming more common as the market evolves toward integrated video processing solutions.

List of Key Video Sync Separator Companies Profiled

Renesas Electronics Corporation (Japan)

Texas Instruments (U.S.)

National Semiconductor Corporation (U.S.)

NTE Electronics (U.S.)

ROHM Semiconductor (Japan)

Maxim Integrated (U.S.)

GENNUM Corporation (Canada)

Intersil Corporation (U.S.)

Segment Analysis:

By Type

Composite Segment Leads the Market Due to Widespread Use in Standard Video Processing

The market is segmented based on type into:

Composite

Subtypes: PAL, NTSC, SECAM

Horizontal

Vertical

Others

By Application

Consumer Electronics Segment Dominates Due to High Demand from Display Manufacturers

The market is segmented based on application into:

Imaging

Consumer electronics

Broadcast equipment

Medical imaging devices

Others

By Protocol

HDTV Segment Growing Rapidly Due to Shift Towards High Definition Content

The market is segmented based on protocol compatibility into:

SDTV

HDTV

NTSC

PAL

SECAM

By End User

Original Equipment Manufacturers (OEMs) Hold Major Market Share

The market is segmented based on end users into:

Original Equipment Manufacturers (OEMs)

Consumer electronics repair services

Broadcast equipment manufacturers

Medical device manufacturers

Others

Regional Analysis: Video Sync Separator Market

North America The North American market remains a dominant player in the video sync separator industry, driven by strong demand from the consumer electronics and imaging sectors. The U.S. alone holds a significant market share, accounting for nearly 40% of global demand in 2024. This is largely due to the proliferation of high-definition broadcasting standards and investments in 4K and 8K display technologies. Major semiconductor manufacturers, including Texas Instruments and Maxim Integrated, are headquartered in the region, accelerating innovation in sync separator ICs. However, market maturity and saturation in core segments pose challenges for aggressive growth. Stringent FCC compliance standards continue to influence product development, pushing the adoption of advanced sync solutions.

Europe Europe’s market benefits from robust demand in automotive infotainment and medical imaging, where precise video synchronization is critical. Germany and the U.K. are leading contributors, aided by a thriving industrial electronics ecosystem. The region is witnessing increased adoption of AI-powered video processing, which relies on high-performance sync separators for latency-sensitive applications. EU regulations on electromagnetic compatibility (EMC) indirectly shape product specifications, creating a preference for compliant chipsets from suppliers like Renesas and NXP. While the market exhibits steady growth, pricing pressures from Asian manufacturers and slow adoption of legacy analog systems restrain expansion.

Asia-Pacific Asia-Pacific is the fastest-growing market, spearheaded by China, Japan, and South Korea, where consumer electronics manufacturing dominates demand. China alone contributes over 30% of global shipments, with local players expanding their footprint in IC design. The rise of smart TVs, surveillance systems, and gaming consoles directly fuels demand for sync separators. Japan remains a hub for high-precision imaging equipment, while India’s burgeoning digital infrastructure projects offer untapped potential. However, intense competition from domestic suppliers and price volatility in the semiconductor supply chain create margin pressures for international players. The region’s shift toward IP-based video transmission could redefine long-term demand for traditional sync solutions.

South America South America presents nascent opportunities, primarily in Brazil and Argentina, where broadcast infrastructure modernization is underway. Local production remains limited, forcing reliance on imports from North American and Asian suppliers. Economic instability and currency fluctuations deter large-scale investments, though niche applications in security systems and educational AV equipment sustain moderate demand. The absence of stringent technical standards results in a fragmented market where both high-end and low-cost solutions coexist. Potential growth hinges on increased digitization of media and telecommunications networks.

Middle East & Africa This region shows gradual growth, led by the UAE and Saudi Arabia, where smart city initiatives and expanding broadcast networks drive procurement of video processing components. The market is highly import-dependent, with suppliers like ROHM and Intersil leveraging distribution partnerships to serve the region. Inconsistent regulatory frameworks and budgetary constraints delay the adoption of cutting-edge technologies, though demand for basic sync separators in surveillance and signage applications remains steady. Long-term prospects hinge on infrastructure development and increased localization of semiconductor assembly.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Video Sync Separator markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Video Sync Separator market was valued at USD 150.2 million in 2024 and is projected to reach USD 225.8 million by 2032, growing at a CAGR of 5.2%.

Segmentation Analysis: Detailed breakdown by product type (Composite, Horizontal, Vertical), application (Imaging, Consumer Electronics, Others), and end-user industry to identify high-growth segments.

Regional Outlook: Insights into market performance across North America (USD 42.5 million in 2024), Europe, Asia-Pacific (fastest growing at 6.1% CAGR), Latin America, and Middle East & Africa, with country-level analysis.

Competitive Landscape: Profiles of leading players including Renesas (18% market share), Texas Instruments (15%), ROHM (12%), Maxim Integrated, and Intersil, covering product portfolios, R&D, and M&A activities.

Technology Trends: Assessment of emerging video processing technologies, integration with AI/ML, and evolving video standards (8K, HDR).

Market Drivers & Restraints: Evaluation of growth drivers (rising demand for high-quality video processing, 5G adoption) and challenges (supply chain constraints, pricing pressures).

Stakeholder Analysis: Strategic insights for semiconductor manufacturers, OEMs, system integrators, and investors.

Related Reports:https://semiconductorblogs21.blogspot.com/2025/06/chip-solid-tantalum-capacitor-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-electrical-resistance-probes.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/high-temperature-tantalum-capacitor.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/global-link-choke-market-innovations.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/multirotor-brushless-motors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/planar-sputtering-target-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ferrite-core-choke-market-opportunities.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/float-zone-silicon-crystal-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/carbon-composition-resistors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/resistor-network-array-market-analysis.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/melf-resistors-market-key-drivers-and.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/metal-foil-resistors-market.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/metal-oxidation-resistors-market-size.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/ferrite-toroid-coils-market-growth.htmlhttps://semiconductorblogs21.blogspot.com/2025/06/vacuum-fluorescent-displays-market.html

0 notes

Text

Float Glass Market

Float Glass Market is forecast to reach $37.79 billion by 2025, after growing at a CAGR of 4.59% during 2020–2025.

🔗 𝐆𝐞𝐭 𝐑𝐎𝐈-𝐟𝐨𝐜𝐮𝐬𝐞𝐝 𝐢𝐧𝐬𝐢𝐠𝐡𝐭𝐬 𝐟𝐨𝐫 𝟐𝟎𝟐𝟓-𝟐𝟎𝟑𝟏 → 𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐍𝐨𝐰

Float Glass Market is a vital segment of the global glass industry, driven by its wide use in construction, automotive, solar energy, and interior design. Produced through a process that yields high optical clarity and uniform thickness, float glass is valued for its durability, versatility, and recyclability. Rising demand for energy-efficient buildings, smart glass technologies, and automotive innovation continues to propel market growth. Asia-Pacific dominates production and consumption, with China and India as key players.

🔹 𝟏. 𝐂𝐨𝐧𝐬𝐭𝐫𝐮𝐜𝐭𝐢𝐨𝐧 & 𝐈𝐧𝐟𝐫𝐚𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞 𝐆𝐫𝐨𝐰𝐭𝐡

Increasing urbanization and infrastructure development, especially in Asia-Pacific, are driving demand for float glass in windows, facades, and interior partitions.

🔹 𝟐. 𝐀𝐮𝐭𝐨𝐦𝐨𝐭𝐢𝐯𝐞 𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧

Growing vehicle production and demand for advanced glazing in windshields and windows are boosting float glass consumption.

🔹 𝟑. 𝐄𝐧𝐞𝐫𝐠𝐲 𝐄𝐟𝐟𝐢𝐜𝐢𝐞𝐧𝐜𝐲 & 𝐆𝐫𝐞𝐞𝐧 𝐁𝐮𝐢𝐥𝐝𝐢𝐧𝐠 𝐈𝐧𝐢𝐭𝐢𝐚𝐭𝐢𝐯𝐞𝐬

Rising focus on sustainable architecture and energy-efficient buildings fuels demand for low-emissivity (Low-E) and solar control float glass.

🔹 𝟒. 𝐓𝐞𝐜𝐡𝐧𝐨𝐥𝐨𝐠𝐢𝐜𝐚𝐥 𝐀𝐝𝐯𝐚𝐧𝐜𝐞𝐦𝐞𝐧𝐭𝐬

Innovations in smart glass, laminated glass, and coated float glass enhance functionality, safety, and aesthetic appeal.

🔹 𝟓. 𝐒𝐨𝐥𝐚𝐫 𝐄𝐧𝐞𝐫𝐠𝐲 𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐆𝐫𝐨𝐰𝐭𝐡

Float glass is essential for photovoltaic panels and solar thermal systems, aligning with the global renewable energy push.

𝐋𝐢𝐦𝐢𝐭𝐞𝐝-𝐓𝐢𝐦𝐞 𝐎𝐟𝐟𝐞𝐫: 𝐆𝐞𝐭 $𝟏𝟎𝟎𝟎 𝐎𝐟𝐟 𝐘𝐨𝐮𝐫 𝐅𝐢𝐫𝐬𝐭 𝐏𝐮𝐫𝐜𝐡𝐚𝐬𝐞

𝐓𝐨𝐩 𝐊𝐞𝐲 𝐏𝐥𝐚𝐲𝐞𝐫𝐬:

Emirates Float Glass LLC | PHP Float Glass Industries Limited | Nasir Float Glass Industries Ltd. | Mediterranean Float Glass MFG | Clear Float Glass | Xinyi Float Glass |

#FloatGlass #GlassIndustry #GlassManufacturing #ArchitecturalGlass #GlassSolutions #ConstructionMaterials #AutomotiveGlass #SolarGlass #SmartGlass #EnergyEfficientGlass

0 notes

Text

Settlement Sensors Market 2025

Settlement sensors are specialized instruments designed for monitoring ground movement and structural displacement in civil engineering projects. These sensors play a crucial role in ensuring safety and stability in large-scale infrastructure projects such as tunnels, dams, embankments, and high-rise buildings. The primary function of settlement sensors is to measure shifts in ground levels due to external forces like excavation, grouting, or natural geological movements.

Get more reports of this sample : https://www.intelmarketresearch.com/download-free-sample/640/global-settlement-sensors-forecast

The maximum measurement range of settlement sensors typically reaches ±30 degrees, making them highly suitable for real-time safety monitoring. These sensors are indispensable in construction and geotechnical engineering, where precise movement detection is necessary to prevent failures and structural instability.

Market Size

The global settlement sensors market has witnessed significant growth over the past few years, driven by increasing infrastructure projects and stringent safety regulations. In 2022, the market was valued at US$ million, and projections indicate a steady increase, reaching US$ million by 2035 at a CAGR of % during the forecast period.

Several factors contribute to this growth, including urban expansion, rising investments in smart cities, and heightened awareness regarding structural safety. The COVID-19 pandemic and geopolitical events, such as the Russia-Ukraine war, have influenced the market dynamics, but the demand for settlement sensors remains resilient due to ongoing construction and maintenance projects worldwide.

Market Dynamics (Drivers, Restraints, Opportunities, and Challenges)

Drivers

Growing Infrastructure Development – Rapid urbanization and government investments in infrastructure projects are fueling the demand for settlement sensors.

Stringent Safety Regulations – Increasing regulations mandating real-time monitoring of construction sites boost the market for these sensors.

Technological Advancements – Innovations in digital settlement sensors and IoT-based monitoring solutions are enhancing market penetration.

Restraints

High Initial Investment – The cost of settlement sensors and associated monitoring systems can be a deterrent for small-scale construction firms.

Limited Awareness in Emerging Markets – The adoption rate in developing regions remains slow due to a lack of awareness and technical expertise.

Opportunities

Smart City Initiatives – The development of smart cities worldwide presents an untapped opportunity for settlement sensor deployment.

Advancements in Wireless and Remote Sensing Technology – The integration of wireless settlement sensors with AI-driven predictive analytics is a growing trend.

Challenges

Environmental Factors – Harsh environmental conditions can impact sensor accuracy and performance.

Data Integration Issues – Ensuring seamless integration with existing monitoring systems can be complex.

Regional Analysis

North America

The U.S. is a dominant player in the settlement sensors market due to its advanced infrastructure, stringent regulations, and adoption of smart monitoring solutions.

Europe

Countries like Germany, the U.K., and France are at the forefront of geotechnical monitoring, driving market demand.

Asia-Pacific

China and India are key contributors due to large-scale construction projects, urbanization, and government-driven infrastructure programs.

South America & Middle East/Africa

Emerging markets in Brazil, Saudi Arabia, and the UAE show growing adoption, driven by infrastructural investments.

Get more reports of this sample : https://www.intelmarketresearch.com/download-free-sample/640/global-settlement-sensors-forecast

Competitor Analysis

The market is competitive, with key players including:

GEOKON

Specto Technology

GEONOR

ENCARDIO-RITE

RST Instruments

Geosense

GEO-Instruments

Cementys

Durham Geo-Enterprises, Inc.

These companies are investing in R&D and strategic partnerships to enhance product offerings.

Market Segmentation (by Application)

Hydraulic Construction

Dams and Embankments

Slope and Excavation Works

Tunnels and Underground Works

Others

Market Segmentation (by Type)

Digital Settlement Sensors

Vibrating Wire Settlement Sensors

Others

Geographic Segmentation

North America (US, Canada, Mexico)

Europe (Germany, France, UK, Italy, Russia, Nordic, Benelux, Rest of Europe)

Asia (China, Japan, South Korea, Southeast Asia, India, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East & Africa (Turkey, Israel, Saudi Arabia, UAE, Rest of Middle East & Africa)

FAQ Section :

1. What is the current market size of the settlement sensors market?

The market was valued at US$ million in 2022 and is projected to grow at a CAGR of % until 2035.

2. Which are the key companies operating in the settlement sensors market?

Major players include GEOKON, Specto Technology, GEONOR, ENCARDIO-RITE, and RST Instruments.

3. What are the key growth drivers in the settlement sensors market?

Infrastructure development, stringent safety regulations, and technological advancements drive the market growth.

4. Which regions dominate the settlement sensors market?

North America, Europe, and Asia-Pacific are the leading regions in market demand.

5. What are the emerging trends in the settlement sensors market? Smart city initiatives, AI-driven predictive analytics, and wireless monitoring solutions are key trends shaping the industry.

This report serves as a valuable resource for investors, researchers, and industry players looking to understand and navigate the settlement sensors market effectively.

Get more reports of this sample : https://www.intelmarketresearch.com/download-free-sample/640/global-settlement-sensors-forecast

0 notes

Link

0 notes

Text

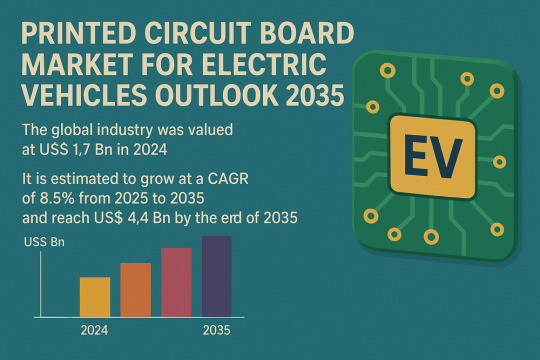

Smart Mobility Drives Smart PCBs: Market to Hit $4.4Bn by 2035

The global Printed Circuit Board (PCB) Market for Electric Vehicles (EVs) is set to witness significant expansion over the next decade, according to the latest market analysis. Valued at US$ 1.7 billion in 2024, the market is projected to grow at a CAGR of 8.5% from 2025 to 2035, reaching a valuation of US$ 4.4 billion by the end of the forecast period.

Market Overview: Printed Circuit Boards (PCBs) are the electronic backbone of electric vehicles, enabling power distribution, connectivity, and control across critical systems such as battery management, motor control, infotainment, and advanced safety features. With EV adoption accelerating globally, PCBs have become essential to the performance, reliability, and innovation of next-generation vehicles.

Market Drivers & Trends

One of the primary drivers of this market is the growing investment and strategic partnerships in the EV supply chain. Leading automakers and electronics companies are heavily investing in R&D and manufacturing capacity to meet the increasing demand for high-performance PCBs.

Moreover, the rise of autonomous and connected vehicles has made sophisticated electronics an indispensable part of modern transportation. The proliferation of features like ADAS (Advanced Driver-Assistance Systems), V2X communication, and in-vehicle infotainment is pushing the demand for compact, multi-layer, high-speed, and thermally efficient PCBs.

In 2023, EV sales in the U.S. surged by 60%, while the European Commission invested over US$ 6 billion in EV infrastructure further stimulating demand for advanced PCB solutions.

Latest Market Trends

The industry is witnessing a rapid shift toward flexible and high-density interconnect (HDI) PCBs, which are crucial for compact and space-saving vehicle designs. Flexible PCBs, in particular, are gaining traction in battery management systems and advanced sensor modules due to their lightweight and adaptable nature.

Additionally, regulatory advancements such as the FCC's allocation of the 5.9 GHz band for vehicle safety and autonomous functions have opened doors for new PCB capabilities. Real-time, high-speed data transmission requires advanced PCB materials and multi-layer configurations.

Key Players and Industry Leaders

Some of the most prominent players shaping the global printed circuit board market for electric vehicles include:

ABL CIRCUITS

AT&S Austria Technologie & Systemtechnik Aktiengesellschaft I

Chin Poon Industrial Co., Ltd.

Compeq Manufacturing Co., Ltd.

HannStar Board Corporation

Kinwong Electronic Co. Ltd

LG Innotek

MEIKO ELECTRONICS Co., Ltd.

Nan Ya Printed Circuit Board Corporation

RayMing PCB

Rush PCB Ltd.

SCHWEIZER ELECTRONIC AG

Shenzhen Capel Technology Co., Ltd.

Shenzhen Fastprint Circuit Tech Co., Ltd.

TTM Technologies

Unimicron Technology Corporation

Victory Giant Technology Co., Ltd.

WUS Printed Circuit Co., Ltd.

Young Poong Group

Zhen Ding Tech. Group

Among Others

These companies are prioritizing innovation, expanding global manufacturing footprints, and forging strategic alliances to maintain competitiveness and cater to evolving industry needs.

Download now to explore primary insights from our Report in this sample - https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=86464

Recent Developments

October 2024 – Mektech Manufacturing announced a 920 million baht investment in Thailand to expand production capacity for flexible PCBs and FPCBA used in electric vehicles.

July 2024 – Omron Electronic Components Europe launched a high-power PCB relay for Level 2 EV charging stations. The innovation features double-break contact designs, enabling reduced heat dissipation and enhanced energy efficiency.

Market Opportunities

The market is poised for significant opportunities, particularly in:

OEM collaborations to co-develop application-specific PCBs for power electronics and smart mobility.

Flexible PCB technology, which is expected to revolutionize EV design with lightweight, customizable circuit boards.

Geographical expansion into regions like South Asia and Latin America, where EV adoption is accelerating, and supply chains are emerging.

Additionally, the ongoing reshoring of PCB manufacturing in regions such as North America and Europe presents untapped potential for local players.

Future Outlook

According to analysts, the convergence of EV electrification, autonomy, and connectivity will demand ever more sophisticated PCB solutions. Next-generation EVs will require PCBs capable of managing 50 Gbps data speeds, robust thermal management, and high signal integrity. Flexible, multilayer, and ceramic PCBs are expected to gain ground rapidly.

As regulations around emissions and vehicle safety become more stringent, automakers will rely heavily on advanced PCB solutions to remain compliant and competitive. From battery optimization to smart in-vehicle systems, the demand for high-performance PCBs is set to skyrocket.

Market Segmentation

The global PCB market for EVs is segmented across several parameters:

By Type: Multilayer (dominant with 73.98% market share in 2024), Double-sided, Single-sided

By Substrate Type: HDI/Micro-via/Build-up, Flexible, Rigid-flex, Rigid 1-2 Sided

By Material: FR4, Metal-Based, Ceramic, PTFE, Power Combi-boards

By Application: ADAS, Battery Management, Powertrain, Lighting & Display, Charging, Connectivity, etc.

By Vehicle Type: Passenger Cars, Buses, Two-Wheelers, Trucks, Off-Highway Vehicles

By End Users: OEMs, Tier 1 & 2 Suppliers, Aftermarket

Regional Insights

East Asia is the undisputed leader in the global market, accounting for 68.3% of the total share in 2024. The region’s dominance stems from:

A well-established electronics manufacturing ecosystem

Government support for EV expansion and green technology

Cost-effective production and high R&D capabilities

Japan, South Korea, and China house the majority of leading PCB suppliers and EV component manufacturers. Their early investment in automation and material innovation is positioning East Asia as the global hub for EV electronics.

Other key regions include:

North America, driven by government initiatives like the CHIPS Act

Europe, focused on sustainable manufacturing and reducing supply chain reliance on Asia

South Asia, emerging as a low-cost, high-volume manufacturing zone

Why Buy This Report?

This in-depth industry report offers:

Detailed market sizing and forecast (2020–2035)

Comprehensive segmentation across product, material, vehicle type, and region

Competitive landscape with profiles of 20+ leading companies

Insights into trends, innovations, and regional dynamics

Strategic recommendations for stakeholders, investors, and policymakers

Whether you're an investor, OEM, component supplier, or policy planner, this report serves as a strategic guide to understanding growth dynamics and identifying emerging opportunities in the PCB market for electric vehicles.

Explore Latest Research Reports by Transparency Market Research: Active Optical Cable Market: https://www.transparencymarketresearch.com/active-optical-cables.html

3D Cameras Market: https://www.transparencymarketresearch.com/3d-cameras-market.html

Optoelectronics Market: https://www.transparencymarketresearch.com/optoelectronics-market.html

Machine Safety Market: https://www.transparencymarketresearch.com/machine-safety-market.html

DC-DC Converter OBC Market: https://www.transparencymarketresearch.com/dc-dc-converter-obc-market.html

About Transparency Market Research Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information. Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports. Contact: Transparency Market Research Inc. CORPORATE HEADQUARTER DOWNTOWN, 1000 N. West Street, Suite 1200, Wilmington, Delaware 19801 USA Tel: +1-518-618-1030 USA - Canada Toll Free: 866-552-3453 Website: https://www.transparencymarketresearch.com Email: [email protected]

0 notes

Text

Global Implantable Defibrillator Market expands with new launches, estimated 7% CAGR by 2030

The global implantable defibrillator market is projected to grow at a CAGR of ~7% during the forecast period. The growth is primarily driven by the rising prevalence of cardiovascular diseases, advancements in device technology, growing geriatric population, and supportive healthcare policies. Increasing investment in healthcare infrastructure and emphasis on reducing sudden cardiac death rates further fuel the market growth. However, the market faces challenges such as high costs of devices and procedures, limited awareness in emerging markets, and risks associated with implantation procedures.

The implantable defibrillator market encompasses the production, distribution, and adoption of devices designed to prevent sudden cardiac death by managing life-threatening arrhythmias. It includes different types of implantable defibrillators such as transvenous, subcutaneous, and wearable models, along with supporting technologies. The market addresses a critical need in cardiovascular care, focusing on individuals at risk of ventricular tachycardia or fibrillation. Growing awareness about heart disease management and technological advancements have made implantable defibrillators an essential component of modern healthcare.

Download a free sample report for in-depth market insight https://meditechinsights.com/implantable-defibrillator-market/request-sample/

Rising cardiovascular disease burden drives implantable defibrillator market

The increasing global prevalence of cardiovascular diseases (CVDs) is a significant driver for the implantable defibrillator market. According to the WHO, an estimated 17.9 million people die each year due to CVDs, accounting for ~32% of all global deaths, with ~85% of these deaths caused by heart attack and stroke. CVDs, including arrhythmias and heart failure, hold the largest share of global mortality, underscoring the urgent need for preventive and therapeutic solutions. Implantable defibrillators are critical in reducing mortality rates by providing real-time monitoring and immediate intervention during life-threatening arrhythmias. Aging populations and lifestyle shifts, such as unhealthy diets, smoking, and physical inactivity, have exacerbated CVD rates. Governments and health organizations are increasingly promoting screening and treatment initiatives, while technological advancements, such as remote monitoring, enhance accessibility and reliability, ensuring sustained growth for this life-saving market.

Transformative innovations elevating implantable defibrillator technology

Technological innovations significantly enhance implantable defibrillators' functionality and appeal, driving market growth. Modern ICDs are increasingly equipped with wireless connectivity and remote monitoring capabilities, enabling healthcare providers to track patient conditions and device performance in real time. Additionally, advancements in miniaturization have led to smaller, more comfortable devices with longer battery life, improving patient compliance and satisfaction.

A major breakthrough in ICD technology is the Extravascular ICD (EV-ICD), which provides a less invasive alternative to traditional transvenous ICDs (T-ICD) while offering pacing capabilities not available in subcutaneous ICDs (S-ICDs). EV-ICDs place leads outside the bloodstream but closer to the heart than S-ICDs, reducing complications associated with transvenous lead implantation while ensuring effective defibrillation. Clinical trials for EV-ICDs have shown promising safety and efficacy results, positioning them as a next-generation solution in cardiac rhythm management.

Furthermore, companies are also integrating AI-driven analytics into ICD systems to improve arrhythmia detection accuracy and personalize treatment strategies. These advancements not only improve patient outcomes but also expand the adoption of ICDs across broader patient demographics, significantly boosting market growth.

Competitive Landscape Analysis

The global implantable defibrillator market features established and emerging players, including Abbott; Medtronic; BIOTRONIK SE & Co. KG; Boston Scientific Corporation; MicroPort Scientific Corporation; and LivaNova PLC among others. Some of the key strategies adopted by market players include product innovation and development, strategic partnerships and collaborations, and geographic expansion.

Unlock key data with a sample report for competitive analysis: https://meditechinsights.com/implantable-defibrillator-market/request-sample/

Market Segmentation

This report by Medi-Tech Insights provides the size of the global implantable defibrillator market at the regional- and country-level from 2023 to 2030. The report further segments the market based on product and end-user.

Market Size & Forecast (2023-2030), By Product, USD Million

ICDs

EV-ICD

S-ICD

T-ICD

Single-chamber

Dual-chamber

CRT-D

Market Size & Forecast (2023-2030), By End-user, USD Million

Hospitals

Ambulatory Surgical Centers

Others

Market Size & Forecast (2023-2030), By Region, USD Million

North America

US

Canada

Europe

UK

Germany

France

Italy

Spain

Rest of Europe

Asia Pacific

China

India

Japan

Rest of Asia Pacific

Latin America

Middle East & Africa

About Medi-Tech Insights Medi-Tech Insights is a healthcare-focused business research & insights firm. Our clients include Fortune 500 companies, blue-chip investors & hyper-growth start-ups. We have completed 100+ projects in Digital Health, Healthcare IT, Medical Technology, Medical Devices & Pharma Services in the areas of market assessments, due diligence, competitive intelligence, market sizing and forecasting, pricing analysis & go-to-market strategy. Our methodology includes rigorous secondary research combined with deep-dive interviews with industry-leading CXO, VPs, and key demand/supply side decision-makers.

Contact:

Ruta Halde Associate, Medi-Tech Insights +32 498 86 80 79 [email protected]

0 notes

Text

Gas Sensors Market Industry, Trends, Share by 2025-2033 | Reports and Insights